Business owners often come across unfamiliar tax terms when starting or managing a company, and “disregarded entity” is one of them.

At first glance, the term can seem confusing, especially if you are not familiar with business tax rules.

However, understanding this is important because it can affect how a business reports income and handles certain tax obligations.

If you are forming a new business or simply looking to learn more about business taxation, knowing the basics of disregarded entities can help you better understand how different entities are treated for tax purposes.

What is a Disregarded Entity?

A disregarded entity is a business that is not treated as separate from its owner for tax purposes.

This means the business’s income, expenses, and profits are usually reported on the owner’s tax return rather than through a separate business tax return.

The term is commonly used in the United States tax system, particularly for single-member limited liability companies (LLCs).

Although the business may be recognized as a separate legal entity, it is “disregarded” for certain federal tax purposes, including self-employment tax obligations, which pass directly to the owner.

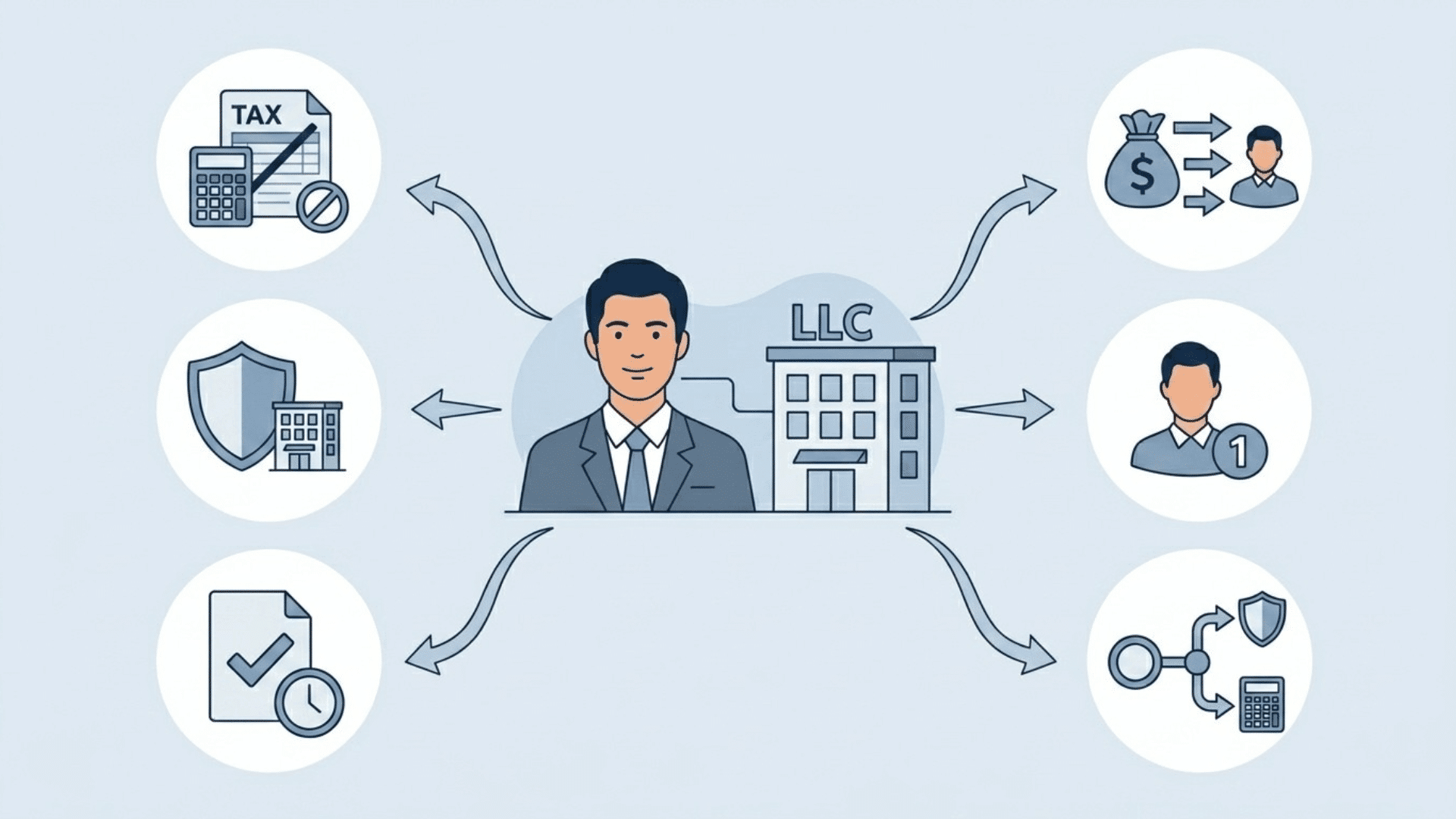

Key Characteristics of a Disregarded Entity

A disregarded entity has several features that set it apart from other business tax classifications.

- Not Treated as a Separate Taxpayer: The owner reports the business’s income and expenses for federal tax purposes.

- Separate Legal Entity in Many Cases: The business can still exist as a separate legal entity under state law.

- Income and Expenses Pass to The Owner: Business profits, losses, and expenses are generally reported on the owner’s tax return.

- Usually Owned by A Single Owner: Most disregarded entities have only one owner.

- Simplified Tax Reporting: Tax filing is often simpler because a separate business tax return is usually not required.

- Different Legal and Tax Status: A business can be legally separate but treated as part of its owner for tax purposes.

Why are Disregarded Entities Used?

Disregarded entities are commonly used because they offer a simple way to handle federal tax reporting.

Instead of filing a separate business income tax return, the owner generally reports the business’s financial activity on their own tax return. This can make tax filing easier and reduce administrative work.

Business owners who also hire staff should be aware that worker classification rules still apply.

Knowing the difference between exempt and non-exempt employees is an important part of staying compliant, regardless of how the business itself is taxed.

In addition, certain entities can still operate as separate legal businesses under state law while using this tax treatment.

As a result, eligible business owners can maintain their chosen business structure without having to file a separate federal income tax return for the entity.

Types of Disregarded Entities

Several types of entities can be treated as disregarded entities. While they have different structures and owners, they share one key feature: they are not treated as separate taxpayers from their owners.

| Type | Ownership | Tax Treatment |

|---|---|---|

| Single-Member LLC | Owned by one individual or one business | The business’s income and expenses are generally reported on the owner’s tax return. |

| Qualified Subchapter S Subsidiary (QSub) | Fully owned by an S corporation | Treated as part of the parent S corporation and not taxed separately. |

| Qualified REIT Subsidiary (QRS) | Fully owned by a Real Estate Investment Trust (REIT) | Treated as part of the parent REIT rather than as a separate taxpayer. |

How Does a Disregarded Entity Work?

A disregarded entity has its own legal structure, but it is not treated as separate from its owner for federal income tax purposes. Here’s a simple look at how it works.

1. The Business Operates as a Legal Entity

A disregarded entity can operate like any other business.

It may enter into contracts, own assets, hire employees, and conduct daily business activities. In many cases, it exists as a separate legal entity under state law.

2. The Business Records Income and Expenses

Like other businesses, a disregarded entity keeps track of the money it earns and the expenses it pays. This includes revenue, operating costs, and other financial transactions throughout the year.

3. The Owner Reports the Business Activity

Instead of filing a separate federal income tax return for the business, the owner generally reports the business’s income, expenses, profits, and losses on their own tax return.

4. The IRS Treats the Owner and Business as One for Tax Purposes

For federal tax purposes, the IRS does not view the entity as separate from its owner, meaning the business’s financial activity is treated as the owner’s.

The IRS provides specific guidance on how this classification works for single-member LLCs.

Owners who hire workers should also understand how classifying someone as a W-2 employee affects their reporting and withholding responsibilities.

Wrapping it Up

Understanding exactly what a disregarded entity is can make it easier to see how certain businesses are treated for tax purposes.

While the rules may seem confusing at first, the main idea is that the owner and the business are often treated as one for federal tax reporting.

This approach can simplify tax obligations for eligible entities while allowing them to operate under their chosen legal structure.