Some employees only think about disability benefits when a health issue affects their work. That is when pay, leave, paperwork, and recovery timelines can start to feel confusing.

The length of benefits is not the same for every employee because coverage may come from an employer plan, a private policy, or a state disability program.

This blog explains how long short-term disability is, what affects the payment period, how state rules differ, and what employees and HR teams should review before a claim starts.

|

Short-term disability usually lasts 3 to 6 months for employer-sponsored plans, though state programs vary; for example, California’s SDI covers up to 52 weeks, while New York and New Jersey cap benefits at 26 weeks. |

What is Short-Term Disability?

This provides partial income when an employee cannot work because of a qualifying non-work-related illness, injury, surgery, or recovery period.

It is usually meant for medical situations that last longer than a few sick days but are not expected to be permanent.

Common qualifying reasons may include surgery recovery, pregnancy and childbirth recovery, serious illness, certain mental health conditions, or non-work-related injuries.

For example, eligible employees may receive disability benefits while also taking protected leave under the Family and Medical Leave Act (FMLA), but the two programs serve different purposes.

Suggested: For a clear breakdown of how these two benefits work together, this guide to short-term disability vs. FMLA explains the key differences and when each applies.

Who Qualifies for Short-Term Disability Benefits?

Eligibility for disability benefits depends on more than simply having a medical condition. Most plans require employees to provide medical documentation and comply with specific policy requirements before benefits begin.

- Covered plan: The employee must be included in an employer plan or insurance policy.

- Qualifying condition: The illness, injury, or medical issue must meet plan rules.

- Unable to work: The employee must be unable to perform essential job duties.

- Medical proof: A licensed healthcare provider must certify the condition.

- Waiting period: Any required waiting period must be completed first.

- Ongoing eligibility: The employee must continue to meet policy requirements during recovery.

How Long is Short-Term Disability?

Although around six months is common for many employer-sponsored plans, it is not a nationwide standard. It is because benefit periods vary across companies and state disability programs.

| Coverage Type | Typical Duration |

|---|---|

| Employer-sponsored plans | 3 to 6 months |

| Private disability insurance | Up to 12 months in some plans |

| State disability programs | Varies by state |

| Pregnancy recovery | Based on medical certification and plan rules |

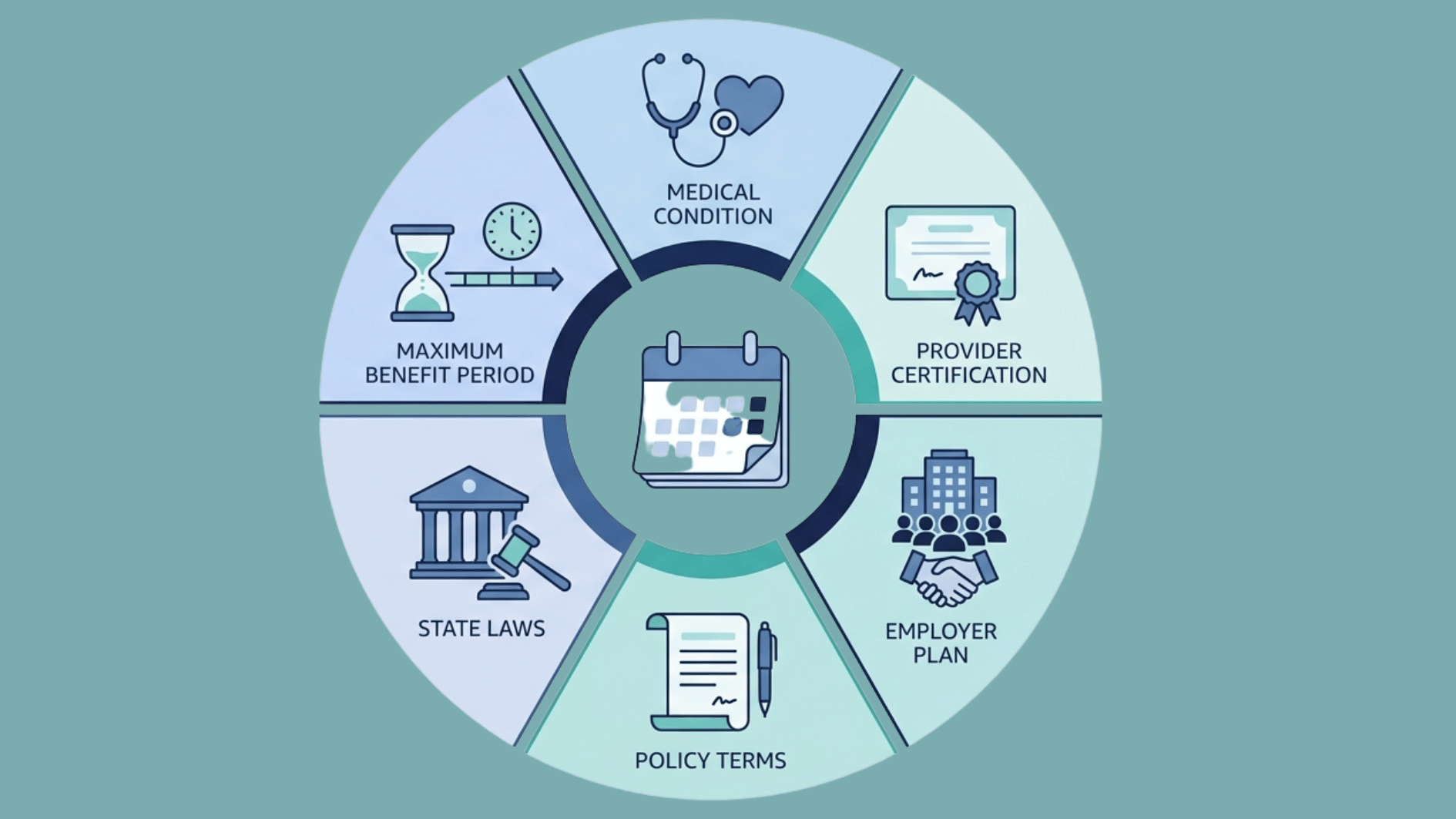

What Determines How Long Benefits Last?

Several factors influence how long short-term disability lasts for a particular employee. Some are based on medical needs, while others depend entirely on the terms of the insurance policy.

- Medical condition: Serious illnesses or surgeries may need longer recovery than minor procedures.

- Provider certification: Benefits usually continue only while a provider confirms the employee cannot work.

- Employer plan: Each employer may set different benefit periods, waiting periods, and coverage rules.

- Policy terms: Private policies define their own eligibility rules and maximum payment periods.

- State laws: Some states set disability benefit rules through public programs.

- Maximum period: Payments usually stop once the policy limit is reached

How Much Does Short-Term Disability Pay?

Benefit amounts vary by employer, insurance company, or state program, but most plans replace a percentage of an employee’s normal earnings rather than their full salary.

Income replacement typically ranges from 40% to 70% of weekly earnings, paid out weekly or biweekly.

The maximum weekly benefit depends on the specific policy or state program, and tax treatment depends on who paid the insurance premium.

State Short-Term Disability Programs in The United States

Not every state requires employers to provide disability benefits. In fact, only a small number of states operate temporary disability insurance programs that provide wage replacement for eligible workers.

1. California State Disability Insurance (SDI)

California offers one of the country’s longest state disability programs through its State Disability Insurance (SDI) program.

Eligible workers may receive benefits for up to 52 weeks if they cannot work because of a qualifying non-work-related illness, injury, or pregnancy.

2. New York Disability Benefits Law (DBL)

New York requires many employers to provide Disability Benefits Law (DBL) coverage to eligible employees who are unable to work due to an off-the-job illness or injury.

Benefits generally last up to 26 weeks within a 52-week period, subject to eligibility, medical evidence, and continued disability.

3. New Jersey Temporary Disability Insurance

New Jersey’s Temporary Disability Insurance program provides partial wage replacement to eligible workers who are temporarily unable to work because of a non-work-related medical condition.

Benefit duration is generally up to 26 weeks, provided eligibility requirements continue to be met.

4. Rhode Island Temporary Disability Insurance

Rhode Island operates one of the oldest state disability insurance programs in the United States.

Eligible employees may receive benefits for up to 30 weeks, depending on their medical condition and program requirements.

5. Hawaii Temporary Disability Insurance

Hawaii requires employers to provide temporary disability insurance that meets state minimum standards. Benefit duration can vary depending on the employer’s approved insurance plan.

The plan must also follow Hawaii’s temporary disability insurance rules and approved coverage requirements.

Benefit amounts, eligibility rules, and payment periods can change over time. Always check your state’s official disability program for the latest information.

Short-Term Disability Vs Long-Term Disability

Both benefits provide income replacement when an employee is unable to work due to a medical condition. The biggest difference is how long benefits last and the type of recovery each plan is designed to support.

|

Feature |

Short-Term Disability | Long-Term Disability |

|---|---|---|

| Purpose | Covers temporary medical leave. | Covers serious or lasting conditions. |

| Start Time | Often starts after 7–14 days. | Often starts after 90–180 days. |

| Duration | Usually lasts 3–6 months. | May last years or until retirement age. |

| Pay | Replaces part of regular income. | Replaces part of regular income. |

| Common Uses | Surgery, pregnancy, illness, injury. | Chronic illness or major disability. |

| Medical Proof | Needs provider certification. | Needs ongoing medical proof. |

| Coverage Source | Employer, private plan, or state program. | Employer or private insurance. |

| End Point | Ends at return or plan limit. | Ends at recovery or policy limit. |

Wrapping it Up

The answer to how long short-term disability lasts depends on the employer’s plan, private insurance policy, or state disability program, which is why benefit periods can range from a few weeks to a year.

Learning about your coverage before you need it can make the claims process much less stressful and help you plan for time away from work with greater confidence.

If your employer offers disability benefits, review your plan documents carefully and, if available, check your state’s disability program to make informed decisions.

Frequently Asked Questions

How Long Is Short-Term Disability for Surgery Recovery?

It depends on the surgery, your recovery, and your disability plan. Benefits often continue until you can safely return to work or until the plan’s maximum benefit period is reached.

What Happens if I Still Cannot Work After Short-Term Disability Ends?

Depending on your situation, you may qualify for long-term disability benefits, employer leave options, workplace accommodations, or Social Security Disability Insurance (SSDI).

Does Pregnancy Qualify for Short-Term Disability?

Many employer plans and some state disability programs cover pregnancy and childbirth recovery when eligibility requirements and medical certification are met.